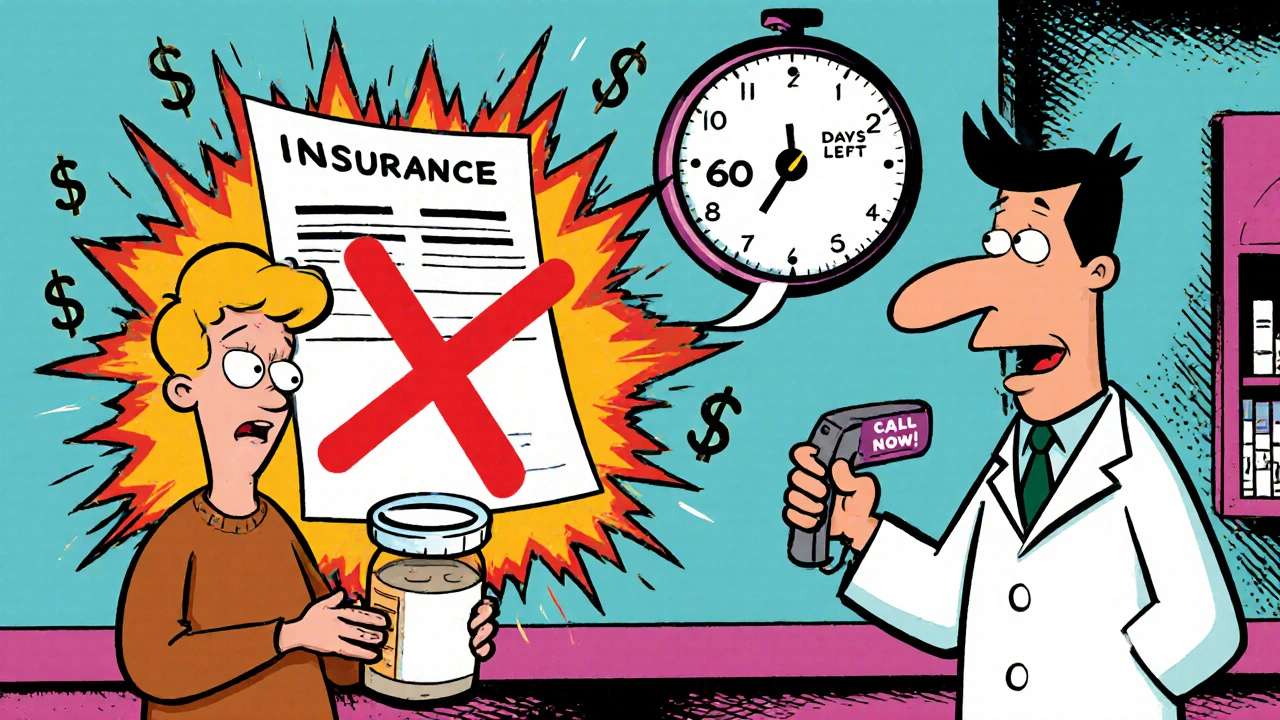

When your insurance plan suddenly stops covering your medication, it’s not just a paperwork issue-it’s a health emergency. Imagine taking Humira for Crohn’s disease for seven years, then waking up one day to find your monthly cost jumped from $50 to $650. That’s not hypothetical. It happened to real people in 2024, and it’s happening every day across Medicare Part D and commercial plans. Formulary changes aren’t rare. They’re routine. And if you don’t know how to respond, you risk stopping your treatment-completely.

What Exactly Is a Formulary?

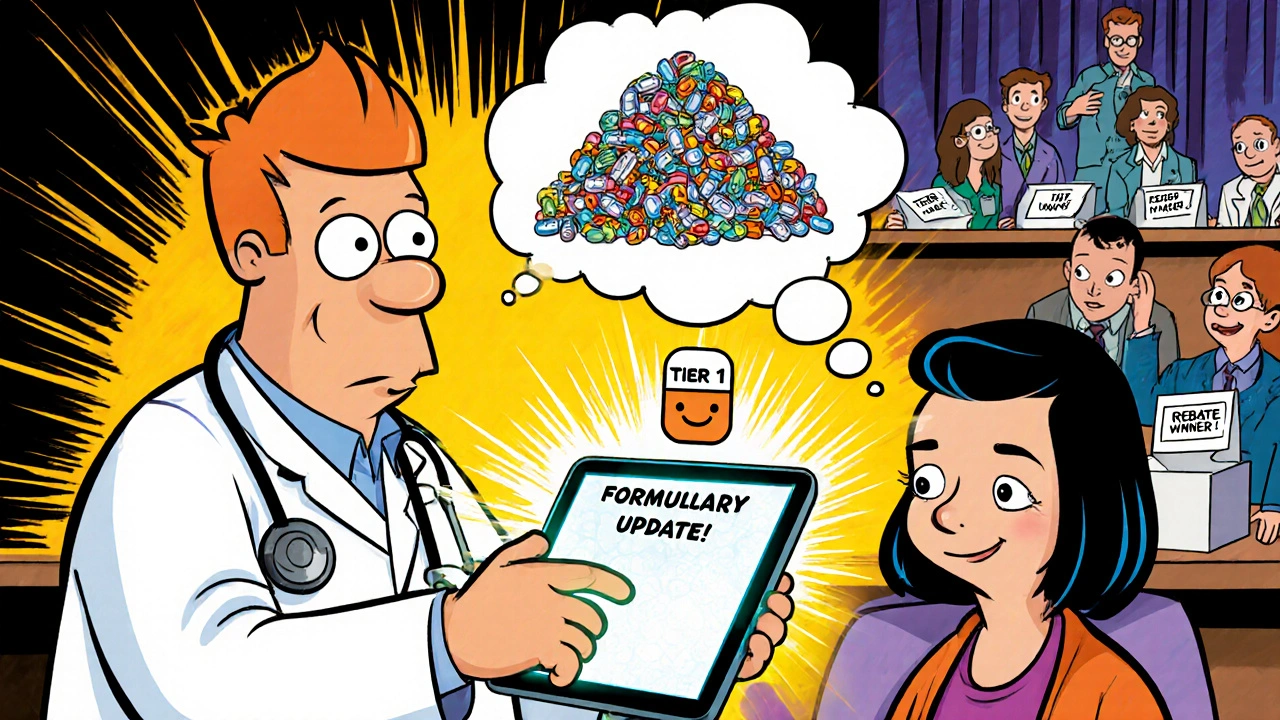

A formulary is a list of drugs your insurance plan agrees to pay for. It’s not just a catalog. It’s a decision engine. Every drug on that list is placed into a tier-Tier 1, Tier 2, Tier 3, or even Tier 6 for specialty meds. Lower tiers mean lower out-of-pocket costs. Higher tiers mean you pay more. Some plans have open formularies (almost everything covered), but 92% of Medicare Part D plans and 87% of commercial plans use tiered systems. That means even if a drug works for you, if it’s not on the right tier, your wallet takes the hit.Why Do Formularies Change?

Formularies change because drug prices rise, new generics hit the market, or manufacturers offer bigger rebates. Pharmacy and Therapeutics (P&T) committees-made up of doctors, pharmacists, and sometimes patients-review new data every quarter. In 2024, 78% of large pharmacy benefit managers (PBMs) updated their formularies at least once every three months. That’s not annual. That’s quarterly. And they don’t always tell you in advance.How Formulary Changes Hurt Patients

When a drug moves from Tier 2 to Tier 3, abandonment rates jump 47%. For diabetes meds? It’s 58%. Why? Out-of-pocket costs. A 2023 Health Affairs study found patients forced to switch drugs paid an extra $587 a year on average. That’s not a small bump. That’s a barrier to care. And it’s worse for people on fixed incomes. A 2024 KFF analysis showed 41% of Medicare beneficiaries didn’t understand why their meds suddenly cost more. The result? Missed doses, ER visits, hospitalizations. Dr. Aaron Kesselheim from Harvard found that excessive formulary restrictions increased emergency visits by 12% among low-income Medicare patients.How Providers Are Managing the Shift

Forward-thinking clinics don’t wait for patients to show up panicked. They use e-prescribing systems that check formulary status in real time. In 2024, 76% of large medical groups did this. That means when a doctor writes a script, the system flags if it’s no longer covered-and suggests an alternative before the patient even leaves the office. It’s not magic. It’s data. And it works. One clinic in Texas cut medication discontinuations by 60% after implementing this. They don’t just react. They anticipate.

What You Can Do: The 60-Day Rule

By law, Medicare plans must give you 60 days’ notice before removing a drug from the formulary. Commercial plans? They only need 30 days-sometimes less. But here’s the trick: you get a grace period. If your drug is being dropped, you can usually get a 30- to 60-day supply to finish your current treatment. Use that time. Don’t wait until your last pill is gone. Start asking questions now.- Call your insurer. Ask: “Is this drug being removed? When? What’s the replacement?”

- Check your plan’s online formulary tool. Most insurers have one. Look up your drug by name.

- Ask your pharmacist. They see formulary changes every day. They’ll know if your drug is still covered or if a generic is now preferred.

Formulary Exceptions: Your Right to Appeal

You don’t have to accept a coverage denial. You can request a formulary exception. This is a formal appeal asking your plan to cover a drug that’s not on the list. In 2023, 64% of medically justified exceptions were approved. You need a letter from your doctor explaining why the alternative drugs won’t work for you. For example: “Patient has tried three generics for rheumatoid arthritis. All caused severe rash. Only biologic X is tolerated.”Medicare vs. Commercial Plans: Know the Difference

Medicare Part D has rules. Commercial plans? Not so much. Medicare must cover at least two drugs per therapeutic class. Commercial plans can drop all but one. Medicare gives you 60 days’ notice. Commercial plans? Sometimes 22 days. Medicare lets you get a 30-day transition supply. Commercial plans? Often don’t. That’s why checking your plan’s formulary during Open Enrollment every fall is critical. Don’t assume your meds are still covered.Manufacturer Assistance Programs Are a Lifeline

If you can’t afford your drug after a formulary change, don’t give up. Drugmakers offer patient assistance programs. In 2024, they covered $6.2 billion in costs for patients. For Humira, AbbVie offers a co-pay card that can reduce your monthly cost to $5. For insulin, Novo Nordisk and Eli Lilly have programs that cap your cost at $35/month. You don’t need to be poor. You just need to ask. Visit the manufacturer’s website. Search “[drug name] patient assistance.” It’s faster than you think.

Therapeutic Alternatives: Not All Are Equal

Your doctor might suggest switching to a different drug. But not all alternatives are created equal. A 2024 JMCP study found that 32% of patients switched to a “therapeutic equivalent” ended up with worse side effects or less control of their condition. Ask your doctor: “Is this alternative proven to work for my specific case?” For example, if you have high blood pressure and your current drug is removed, don’t just take the first generic. Ask if it’s been tested in patients with your kidney function or age group. Sometimes, the cheaper option isn’t the right one.What’s Changing in 2025?

The Inflation Reduction Act kicks in. Starting January 1, 2025, Medicare beneficiaries won’t pay more than $2,000 a year for prescriptions. That’s huge. It means insurers will have to rethink how they structure tiers. Drugs that were previously in the highest tier might drop down. But it also means insurers might push harder to get you on cheaper drugs earlier. Expect more step therapy-requiring you to try two or three cheaper drugs before they’ll cover the one you need.Final Checklist: What to Do Now

- Review your plan’s formulary before November 30, 2025-before Open Enrollment ends.

- Write down every medication you take, including over-the-counter ones your doctor approved.

- Call your insurer or log in to their website. Search each drug. Note the tier and any prior authorization rules.

- If something changed, ask for a formulary exception letter template from your doctor’s office.

- Set a reminder: check your formulary every six months, not just once a year.

- Save the phone number for your State Health Insurance Assistance Program (SHIP). They help free of charge.

When to Seek Help

If you’ve been denied a formulary exception and your condition is worsening, contact your State Health Insurance Assistance Program (SHIP). They’re trained to walk you through appeals. If you’re on Medicare, you can also call 1-800-MEDICARE. For commercial plans, your employer’s HR department might have a benefits advocate. Don’t suffer in silence. You have rights. Use them.What happens if my insurance stops covering my medication?

Your insurer must give you notice-usually 30 to 60 days. During that time, you can request a formulary exception, ask your doctor for a therapeutic alternative, or apply for manufacturer assistance. You may also qualify for a 30- to 60-day transition supply to avoid interruption. Don’t stop taking your medication without a plan.

Can I switch to a different plan if my drug is dropped?

Yes-but only during Open Enrollment (October 15 to December 7 for Medicare) or if you qualify for a Special Enrollment Period due to a life event like moving or losing other coverage. Outside those windows, switching plans won’t help. Your best bet is to appeal the change or find a lower-cost alternative.

Why do some drugs cost more even if they’re the same?

Even if two drugs are chemically identical, insurers may cover one as a preferred generic and not the other. This is often due to rebate deals between the drugmaker and the pharmacy benefit manager. The cheaper-looking drug isn’t always the better choice-it’s just the one the insurer got paid to promote.

How do I know if a drug is on my formulary?

Check your insurer’s website. Most have a formulary search tool. Enter your drug’s name and look for its tier (Tier 1, 2, etc.) and whether prior authorization is required. If you’re on Medicare, use Medicare’s Plan Finder tool. If you’re unsure, ask your pharmacist-they have real-time access to your plan’s rules.

Are there free resources to help me navigate formulary changes?

Yes. State Health Insurance Assistance Programs (SHIP) offer free, personalized help to Medicare beneficiaries. For commercial plans, your employer’s HR department or patient advocacy groups like the Patient Advocate Foundation can guide you. Nonprofits like NeedyMeds and RxAssist also list manufacturer assistance programs.

Ross Ruprecht

November 22, 2025This is such a long post I didn’t even finish reading it but I’m pretty sure I’m gonna get hit with a formulary change next month and I’m already panicking.

Linda Rosie

November 22, 2025Thank you for this clear, factual guide. It’s exactly what patients need when they’re blindsided by cost spikes.

Vivian C Martinez

November 23, 2025As a nurse, I see patients skip doses or stop meds entirely because they can’t afford the new price. This guide should be handed out at every pharmacy.

Bryson Carroll

November 24, 2025Who cares about formularies anyway? Big Pharma and PBMs are just milking the system and everyone’s too lazy to fight back. I stopped taking my meds last year and my health didn’t get worse

Jennifer Shannon

November 24, 2025You know, I’ve been thinking about this for years - the way our healthcare system treats medication like a commodity instead of a lifeline… it’s not just broken, it’s morally inverted. We’ve normalized the idea that someone’s ability to stay alive should hinge on whether their insurer struck a deal with a pharmaceutical company’s sales rep. And yet, we don’t protest. We just pay. Or we suffer. Or we switch. Or we die quietly. The fact that we’ve built entire bureaucratic systems around this cruelty - tiered formularies, prior authorizations, 30-day grace periods - it’s like we’ve turned medicine into a game of musical chairs where the music stops and the chair gets taken away by a spreadsheet.

And yet, we still don’t scream. We just Google ‘patient assistance programs’ like it’s a magic spell. We call SHIP. We beg our doctors to write letters. We wait. We hope. We pray. But no one’s fixing the system. We’re just learning to survive inside it.

I remember when my mom had to switch from Humira to a biosimilar. She cried in the car after the appointment. Not because it was expensive - she had the co-pay card - but because she felt like a burden. Like her body had become a liability to the system. And that’s the real cost. Not the $650. The shame.

Suzan Wanjiru

November 25, 2025Don’t forget to check if your drug has a generic version that’s preferred - sometimes it’s the same thing just cheaper. Pharmacist can tell you right away. Also save the manufacturer’s patient help number - they’ll mail you free samples if you ask.

Kezia Katherine Lewis

November 26, 2025The P&T committee’s decision-making framework is predicated on cost-effectiveness analyses derived from real-world evidence and pharmacoeconomic modeling - but patient-reported outcomes are often underrepresented in these deliberations. Consequently, therapeutic substitution may yield suboptimal clinical trajectories despite formulary compliance.

Henrik Stacke

November 28, 2025Oh my goodness, this is so important - I’ve seen friends lose their jobs, lose their insurance, and then lose their health because they didn’t know about the 60-day rule. This isn’t just medical advice - it’s survival guidance. Thank you for writing this with such clarity.

Manjistha Roy

November 29, 2025Many people in developing countries struggle with access to even basic medications, so when I read about formulary changes in the U.S., I’m reminded how privileged we are to even have options like patient assistance programs. Still, the system should not require patients to become advocates just to stay alive.

Jennifer Skolney

November 30, 2025My dad just got hit with a $400 spike on his blood pressure med last month - we applied for the co-pay card and got it down to $5. Seriously, just call the drug company. They’re not going to come knocking. You have to ask. 💪

JD Mette

December 1, 2025I’ve been on the same med for 12 years. Last year they switched me to a generic I couldn’t tolerate. I didn’t say anything at first. Thought I’d tough it out. Ended up in the ER. I wish I’d known about exceptions sooner.

Olanrewaju Jeph

December 1, 2025This is excellent. In Nigeria, we don’t have formularies - we have availability. If your drug is in stock, you buy it. If not, you find a workaround. The fact that you have systems - even flawed ones - to appeal and negotiate is a privilege. Thank you for sharing this knowledge.